Why this matters now

Many early-stage founders hear this sentence after a good pitch: “We like it, but it’s too early.”

It sounds polite.

It sounds vague.

And it often feels like a soft no.

But in most cases, it’s neither.

This phrase usually means interest without readiness. The investor sees potential. They just don’t see enough risk reduced yet. Understanding what sits behind this feedback can save founders months of frustration — and help them come back stronger.

The common founder assumption

When founders hear “too early”, they often assume:

-

- “They want more traction”

-

- “They only invest later”

-

- “We need to be bigger”

-

- “They didn’t really get it”

Sometimes that’s true. But more often, “too early” is not about size. It’s about unanswered questions.

Investors don’t look for perfection. They look for risk. And at early stage, risk shows up in very specific ways.

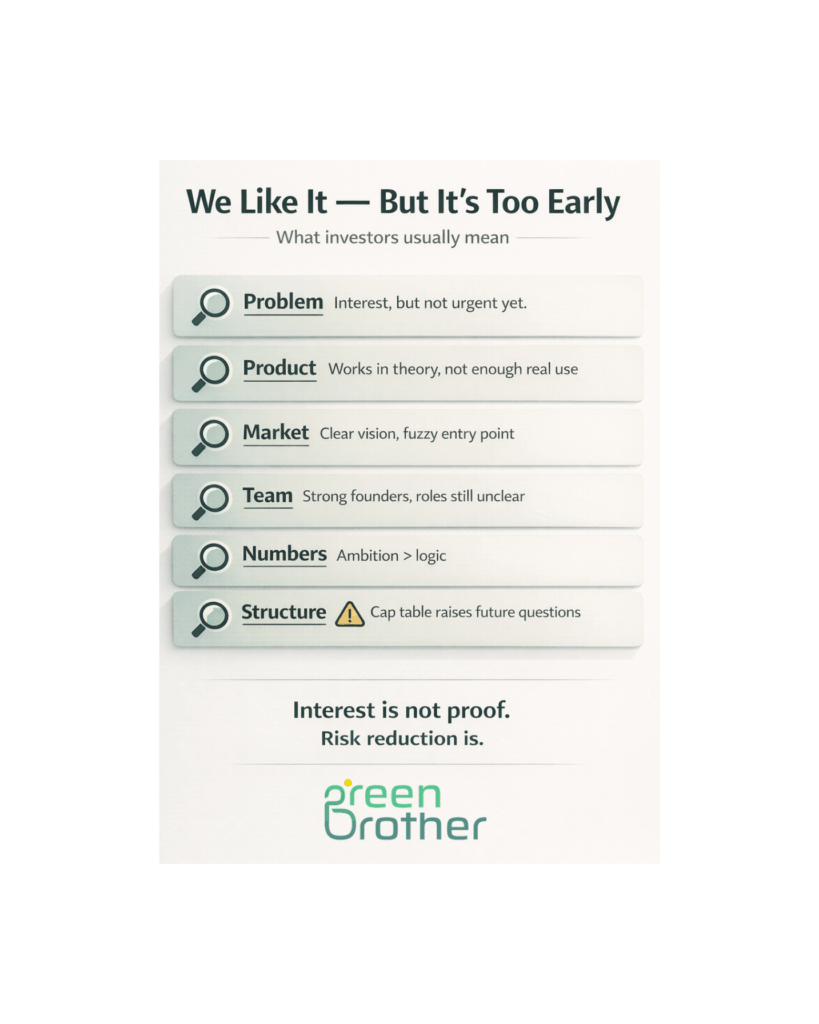

What investors are really saying

When an investor says “too early”, they usually mean one (or more) of these things: “I don’t yet have enough evidence to defend this decision to myself or my partners.” Below are the most common signals behind that sentence.

1. The problem feels real — but not urgent yet

🔍 What investors review

-

- How painful the problem is

-

- Whether customers actively seek solutions

-

- If the pain triggers budget, time, or switching behavior

⚠️ Early-stage risk

-

- Strong interest, weak urgency

-

- “Nice to have” disguised as “must have”

-

- Positive feedback without consequences

Many founders confuse interest with demand.

Interest is people saying:

“That’s interesting.”

Demand is people saying:

“We need this now.”

Interest is not proof.

✔ What “good enough” looks like early

-

- Users pushing to pilot

-

- Clear workflow dependency

-

- Willingness to change behavior

-

- Even small payments or strong LOIs

You don’t need scale. You need pressure.

2. The solution works — but only in theory

🔍 What investors review

-

- Evidence the product works outside a demo

-

- Feedback from real usage

-

- What breaks under real conditions

⚠️ Early-stage risk

-

- Too much vision, not enough reality

-

- Product tested only by the team

-

- No uncomfortable feedback yet

Investors worry when everything sounds smooth. Real usage is messy. And that’s exactly what they want to see.

✔ What “good enough” looks like early

-

- A scrappy MVP in use

-

- Clear learnings from failures

-

- Honest limits of the current product

Early-stage doesn’t mean unprepared.

3. The market story is promising — but still fuzzy

🔍 What investors review

-

- Who exactly buys

-

- Why now

-

- Why this market, not another

-

- How big this specific entry point is

⚠️ Early-stage risk

-

- Market slides that feel generic

-

- TAM without a clear first wedge

-

- Too many use cases at once

Investors don’t fund markets. They fund entries into markets.

✔ What “good enough” looks like early

-

- One clear customer profile

-

- One clear use case

-

- One clear reason why timing matters now

Clarity beats ambition at this stage.

4. The founders are strong — but still untested together

🔍 What investors review

-

- Role clarity

-

- Decision ownership

-

- How conflict is handled

-

- Commitment level

⚠️ Early-stage risk

-

- Overlapping responsibilities

-

- Missing key roles “for later”

-

- Founders who haven’t worked under pressure together

Investors back teams, not slides.

✔ What “good enough” looks like early

-

- Clear division of roles

-

- Honest gaps acknowledged

-

- Evidence of working through real stress

Governance is not bureaucracy. It’s leverage.

5. The numbers exist — but the logic doesn’t yet

🔍 What investors review

-

- Assumptions behind revenue

-

- Sales cycles

-

- Cost drivers

-

- Unit economics directionally

⚠️ Early-stage risk

-

- Forecasts that assume everything goes right

-

- Growth without effort

-

- Pricing without proof

At early stage, numbers are guesses. But the thinking behind them must be solid.

✔ What “good enough” looks like early

-

- Simple model

-

- Clear assumptions

-

- Willingness to say “we don’t know yet”

Confidence grows from realism.

6. The round structure raises future questions

🔍 What investors review

-

- Cap table cleanliness

-

- Founder ownership and incentives

-

- Ability to raise the next round

⚠️ Early-stage risk

-

- Too many small early investors

-

- No vesting

-

- Heavy dilution too soon

A messy foundation slows everything later.

✔ What “good enough” looks like early

-

- Clear ownership

-

- Room for future investors

-

- Aligned founder incentives

Prepared founders move faster.

What “too early” usually means — in one sentence

“I’m interested, but I can’t underwrite the risk yet.” That’s not rejection. That’s a signal.

A simple founder checklist

Before your next round, ask yourself:

🔍 Can we show real user pressure, not just interest?

🔍 Is the product tested in the real world?

🔍 Is our market entry crystal clear?

🔍 Are founder roles and incentives obvious?

🔍 Do our numbers reflect reality, not hope?

🔍 Would a new investor understand our cap table in 5 minutes?

⚠️ If two or more answers feel weak, the feedback makes sense.

Fixing this early is a strength — not a failure.

Calm closing takeaway

“We like it, but it’s too early” is not a dead end. It’s a mirror. It shows where belief exists — and where trust still needs work.

Fundraising doesn’t fail in the pitch. It fails after it. Fix this early — fundraising gets easier.

Important notice: This is educational content, not legal or financial advice.

Coming next:

In our next blog post, we’ll cover how founders can come back after hearing “too early”.

What to fix first, what to ignore, and how to re-engage investors without starting from zero.

Stay tuned!