Why this matters now

Across the EU and CEE startup ecosystem, something subtle has been happening over the past few years. As early-stage founders try to prove traction earlier and earlier, documents like LOIs and MoUs have become standard in pitch decks. You’ve probably seen (or used) slides like these:

“12 LOIs signed”

“3 MoUs with large corporates”

“Strong investor interest”

On the surface, these feel like progress. And in many ways, they are. But here’s the nuance most founders only discover during fundraising: not all signals are created equal—and not all investors read them the same way. A VC does not interpret an LOI the way a corporate investor does. This mismatch goes unnoticed for a while, and things don’t usually break during the pitch.

The Common Founder Assumption

Many founders believe: “We have LOIs, so we are validated.” “A big corporate signed an MoU, that proves demand.” “Investors showed interest, so the round is progressing.” All of these are reasonable.

But investors are trained to separate something founders often mix together: interest and proof. Interest is curiosity.

Proof is commitment. And those are not the same thing. Let’s go deeper into the background.

How VCs Read Signals 🔍

If you step into the mindset of a VC, their lens becomes clearer. They are not investing to integrate your solution into their operations. They are investing because they believe your company can grow fast, scale, and deliver returns in future rounds. So when a VC sees an LOI or an MoU, they are not asking “Is this exciting?” They are asking:

- Will this turn into revenue?

- How quickly?

- Can this be repeated across many customers?

- Or is this just one-off interest?

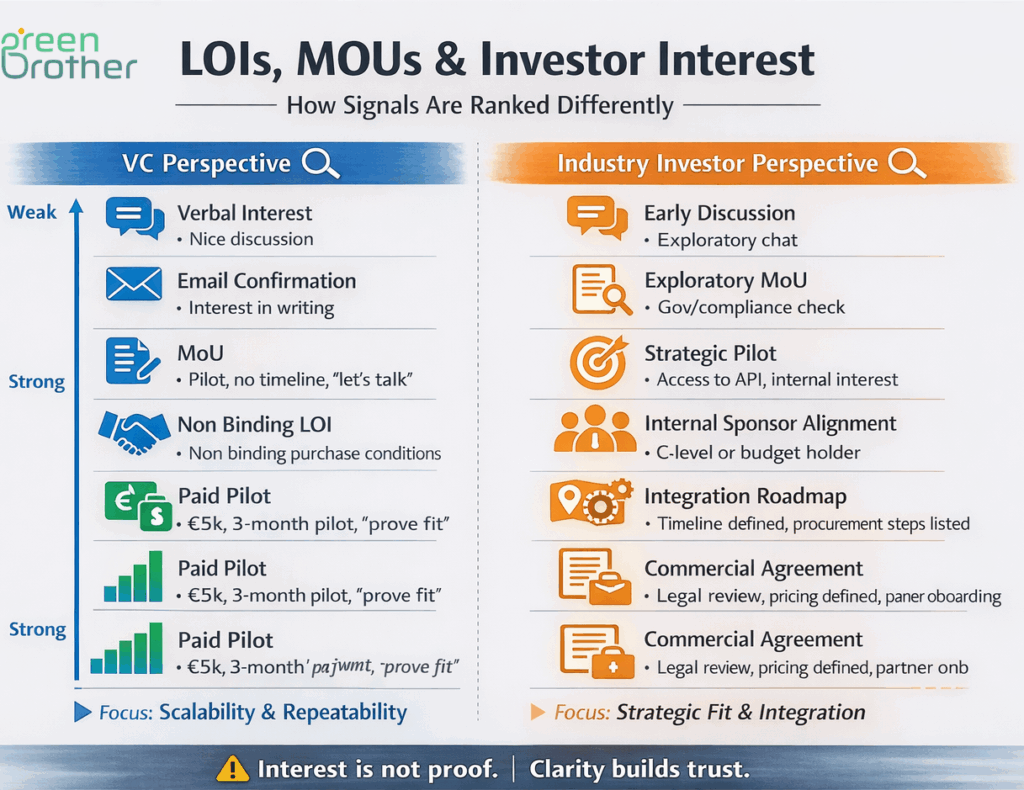

From that perspective, most early traction signals fall into a rough hierarchy.

At the bottom, you have verbal enthusiasm—great for morale, but impossible to measure. An email confirmation is slightly better, but still informal. An MoU shows that conversations are structured. It suggests alignment, but usually remains exploratory. A non-binding LOI feels more serious, it signals intent but still carries no obligation.

Things only start to become truly meaningful when money or internal commitment enters the picture. A paid pilot indicates that someone allocated budget and pushed this through internally. And recurring revenue – even at a small scale – starts to show something VCs deeply care about: repeatability. That’s the core of it.

A single impressive logo rarely moves a VC unless it proves a pattern that can be replicated. They are not looking for perfect traction, they are looking for reduced uncertainty. If your signal helps them believe revenue can scale, it matters.

If it only shows enthusiasm, it doesn’t.

How Industry and Corporate Investors see the same picture differently 🔍

Now shift perspective again. This time into a corporate or industry investor. Their priorities are fundamentally different. They are not just asking, “Can this scale?” They are asking, “Does this fit us?”

They look at:

- Strategic alignment

- Technology fit

- Integration feasibility

- Competitive advantage

- Long-term positioning

- Revenue still matters—but often as a second step.

So the exact same document can carry a completely different weight.

An MoU, which a VC might treat as weak, can be highly meaningful for a corporate if it reflects real partnership alignment. A pilot is not just a revenue signal, it’s proof that integration works in practice. An LOI might indicate that someone inside the organisation is actively pushing this forward.

Their questions are different:

- Can we integrate this into our systems?

- Does it strengthen our market position?

- Is there internal buy-in?

- Who is championing this internally?

In some cases, a corporate investor will value one deeply integrated partner far more than ten small paying customers. A VC might think exactly the opposite.

Where things quietly go wrong

Most fundraising challenges around this topic and they are not legal problems, but they are narrative problems. Nothing “breaks” dramatically but something doesn’t add up, and investors start to hesitate. It often shows up in subtle ways.

Sometimes founders unintentionally inflate what they have—calling early conversations “secured partnerships.” That might pass in a pitch, but it gets tested in due diligence.

Other times, founders confuse strategic validation with market validation. A corporate pilot might prove technical feasibility but not scalable demand.

Big logos can also create a false sense of strength. They look impressive on slides, but investors ask: Who actually signs? Where is the budget? What is the timeline? What is the probability this converts? If the answers are unclear, the signal weakens—no matter how strong the logo looks.

Another common issue is missing conversion logic. Ten LOIs sound impressive, but without a clear path and timeline to conversion, they introduce uncertainty rather than reduce it.

And then there is the word “interest.” It sounds positive but in investor language, it often translates to early-stage curiosity. And curiosity does not fund rounds.

What “good enough” actually looks like

The good news is: you don’t need perfect traction. You need clarity. For VCs, “good enough” often looks surprisingly simple:

- A handful of paying customers or serious pilots.

- A clear understanding of your sales cycle.

- Knowing exactly who makes the decision.

- A realistic view of conversion probability.

- And early signs that what worked once can work again.

The story they want to believe is straightforward: This works and it can be repeated.

For corporate or industry investors, the bar looks different. Sometimes one strong strategic pilot is enough—if it is backed by a senior internal sponsor, demonstrates real technical feasibility, and has a clear path toward commercialisation.

Here, the story is not about scale first. It is about fit: This makes sense for us. And it strengthens our position.

A simple way to sense-check your signals

Before you walk into a pitch, it helps to step back and ask a few grounding questions:

- What exactly has been signed?

- Is it binding or not?

- Who inside the organisation is actually backing this?

- Is there real budget behind it?

- What is the realistic chance this converts?

- And most importantly: can this be repeated?

There’s one test that rarely fails: If you removed the logo, would the signal still feel strong? If yes, you probably have substance. If no, you might be relying more on branding than traction.

Final thought

LOIs and MoUs are not meaningless. But they are often misunderstood. VCs read signals through the lens of scalability. Industry investors read them through the lens of strategic fit.

Your role as a founder is not to inflate traction. It’s to interpret it correctly for your audience. Because in the end, fundraising is not just about what you have. It’s about how clearly you can explain what it actually means.

Clarity builds trust. Trust unlocks capital. And founders who understand this move faster.

Coming next:

In our next blog post, we’ll cover Founder background checks.

Stay tuned!