Why this matters now

Something has shifted in the EU and CEE startup ecosystem. Background checks on founders, once a loose formality, have grown into something far more structured. Cross-border rounds are more common. Institutional and public-backed capital is flowing in. Compliance expectations have risen alongside it.

And yet, a surprising number of early-stage founders still treat the background check as admin. A box-ticking exercise. Something their lawyer handles while they focus on the real work. It isn’t admin. And it isn’t a formality.

Most rounds that fall apart don’t collapse because of the product. They collapse because of trust. And trust, it turns out, is tested quietly, long before anyone tells you the answer.

The assumption most founders make

Ask a founder what investors are checking, and you’ll hear some version of the same four things: criminal records, LinkedIn accuracy, references, and standard paperwork. That’s not wrong, exactly. It’s just incomplete.

What investors are actually doing is assessing risk. Not looking for perfection, not expecting a spotless record, but scanning for patterns that suggest this founder might become a problem twelve, eighteen, or thirty-six months from now. The real question they’re trying to answer is simple: is this person a trustworthy long-term partner for capital? The answer looks different depending on who’s sitting across the table.

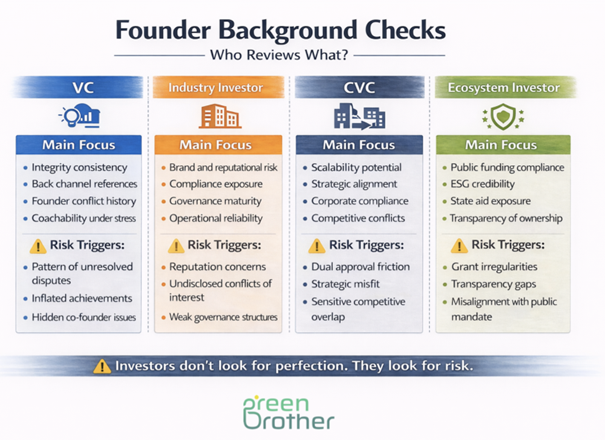

What a traditional VC is really looking for

Venture capitalists don’t evaluate founders through a reputation lens. They use a risk lens. What matters isn’t how polished your profile looks, it’s whether there are patterns in your history that suggest future volatility.

Story consistency comes first. Does your CV match your pitch deck? Do the timelines hold up? Are the roles described clearly? Small inconsistencies, the kind you’d barely notice in conversation, can quietly erode confidence in a way that’s hard to recover from.

Then come the back-channel calls, the ones you’ll never be on. Former co-founders, early employees, previous investors, accelerator managers. VCs ask them variations of the same questions: how does this person behave under stress? Do they take responsibility? Do they share credit? How do they handle conflict when things go wrong?

Financial history matters too, but perhaps not in the way founders expect. A past bankruptcy won’t automatically end a conversation. A hidden one will. Transparency is valued more than perfection.

And finally, pattern recognition around conflict. Have you left multiple ventures under dispute? Is there a trail of broken partnerships? Investors understand that early-stage startups are difficult and messy. What they’re looking for is evidence of emotional resilience and the capacity to be coached. Early stage doesn’t mean unprepared.

What corporate and strategic investors check

Corporate and strategic investors work from a different checklist. Growth matters, yes, but so does something that pure VCs weigh less heavily: brand protection.

Their underlying questions are about fit and risk to their own reputation. Could this founder create a headline problem? Can they represent us publicly in a way we’d be comfortable with? Are there compliance red flags? Is the governance structure mature enough for us to stand behind?

Internal compliance teams will often run their own reviews, covering sanctions lists, conflict of interest exposure, non-compete agreements, and employment restrictions. These processes can feel bureaucratic from the outside, but they reflect a real concern: for a large corporation, a reputational problem attached to a portfolio company isn’t just inconvenient. It’s a liability.

A brilliant founder who attracts attention for the wrong reasons simply isn’t attractive to this type of investor, regardless of the technology.

What CVCs check

Corporate Venture Capital sits between these two worlds, which means it inherits scrutiny from both. A CVC team combines the growth logic of a venture fund with the compliance culture of a large organisation and the strategic priorities of a business unit. That’s three different filters, often running simultaneously.

They evaluate scalability and strategic fit, but also governance maturity, political sensitivity within their parent company, and potential competitive conflicts. The process is often slower than founders expect, and that slowness is frequently misread as hesitation or lack of interest. More often, it’s internal risk filtering working through its own timeline.

What ecosystem investors check

Public-backed and EU-linked investors, organisations like EIT Urban Mobility or InnoEnergy, add another dimension entirely. These are institutions that combine investment logic with public accountability, ESG mandates, state aid compliance, and governance standards.

They may look at how previous grants were used, whether there are overlaps with other public funding, conflict of interest exposure, ESG credibility, the diversity and transparency of the governance structure, and how the cap table is documented. Public capital carries public scrutiny. Founders working with these organisations need to be prepared for a depth of documentation that goes well beyond a typical VC process.

What quietly blocks rounds

Most founders don’t fail background checks because of serious misconduct. They fail because of inconsistency, or because something was left out. The patterns that quietly kill deals tend to look like this: advisory roles described as executive positions, unclear exits, overstated traction. Early contributors with equity claims who were never formally acknowledged. IP that was built by a contractor or early developer without a proper assignment agreement. A parallel business in a similar sector that was never mentioned. A former co-founder who, when called, has something unflattering to say. A small, unresolved tax or legal issue that was never cleaned up.

Fundraising doesn’t fail in the pitch room. It fails in the weeks after it, when inconsistencies surface during due diligence and trust begins to quietly erode.

What “good enough” actually looks like

You don’t need a spotless history. You need a transparent one. For early-stage founders, good enough typically means a clean and understandable CV, honest explanations of any failures, clear IP ownership, a simple and transparent cap table, no hidden liabilities, two or three credible references, and no unresolved legal disputes.

If there’s a weakness somewhere, the right move is to surface it early and explain it clearly. Proactive transparency is almost always received better than a surprise discovered mid-process.

A checklist before you start fundraising

Before approaching investors, it’s worth sitting with these questions honestly:

Is my CV fully aligned with reality? Are all timelines consistent? Are there unresolved founder conflicts that might surface? Do we clearly own all our IP? Would the people I’ve worked with before recommend me without hesitation? Is there anything that could surprise an investor once diligence begins?

If you hesitate on any of these, that hesitation is worth paying attention to. Fix it before you start. Prepared founders move faster, not just through diligence, but through the entire fundraising process.

A final thought

Background checks aren’t designed to catch criminals. They’re designed to measure long-term trust.

VCs focus on behavioural patterns and consistency. Corporates focus on reputational and governance risk. CVCs apply both lenses. Ecosystem investors add public accountability on top of all of it.

The founders who move through this process most smoothly aren’t necessarily the ones with the cleanest histories. They’re the ones who understand what’s being assessed, and who’ve done the work to make sure nothing comes as a surprise.

Clarity builds trust. Trust unlocks capital.

In our next blog post, we”ll explore what investors mean by team risk.

Stay tuned!